This blog distils the key trends, driving forces, and forward-looking signals from recent real estate research and expert conversations, including perspectives shaped by practitioners like Ashwinder R. Singh, whose cross-sector background spanning banking, development, and capital markets offers a useful lens for reading markets like Hyderabad. Whether you're a homebuyer, investor, or developer, the patterns emerging here have direct implications for how you make decisions.

Key Takeaways

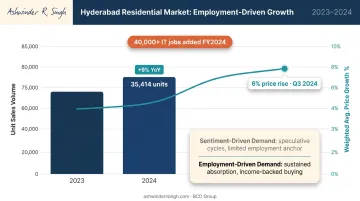

- Hyderabad's IT sector added over 40,000 jobs in FY2024, driving housing demand on employment fundamentals rather than speculative cycles

- Infrastructure corridors — metro, ORR, Financial District — are repricing previously undervalued micro-markets

- Premium homes above ₹1 crore now account for 71% of Hyderabad sales (H2 2025), signalling a structural shift in buyer profiles

- PropTech adoption is accelerating across Hyderabad's market, reshaping how investors evaluate and transact in real estate

- Hyderabad's progressive FSI framework gives it a structural affordability edge over Mumbai and Bengaluru

Trend 1: IT and Knowledge Economy Fuelling Sustained Residential Demand

Hyderabad's residential market is driven by payrolls, not sentiment.

Telangana's IT exports rose 11% to ₹2.68 lakh crore in FY2023-24, with the sector supporting over 9.46 lakh professionals and adding more than 40,000 jobs in that year alone. HITEC City, Gachibowli, and the Financial District remain the employment anchors, but the ripple effects now extend well beyond those corridors.

Dual-Income Households Reshaping the Product Mix

The rise of dual-income professional households — both partners employed in IT or knowledge-sector roles — is doing two things simultaneously:

- Pushing average ticket sizes upward, with the ₹2–5 crore segment seeing an 85% year-on-year jump in 2024 across India's top cities, with Hyderabad a key contributor

- Shifting preference away from compact 2BHK units toward larger, better-amenitised homes where space, functionality, and community infrastructure matter

The data supports this shift. In a Knight Frank registration snapshot, units in the 1,000–2,000 sq ft range accounted for 70% of Hyderabad transactions — a profile consistent with 3BHK and larger 2BHK demand among professional buyers.

Why This Demand Is Different

Most markets move through demand cycles — enthusiasm, then correction. Hyderabad's housing absorption holds steadier because it follows employment growth rather than broader market sentiment.

Hyderabad residential sales reached 35,414 units in 2024, up 9% year-on-year, with weighted average prices rising 6% in Q3 2024. That growth reflects a steady intake of skilled professionals seeking homes near their workplaces — a pattern that persists even when national sentiment softens.

Trend 2: Infrastructure Growth Unlocking New Investment Corridors

Infrastructure is the earliest and most reliable signal of where real estate value will migrate. In Hyderabad, that signal is unusually clear right now — driven by two intersecting forces: metro expansion reaching previously peripheral zones, and Grade A commercial leasing concentrating demand in specific western corridors.

Metro Expansion and Peripheral Connectivity

The Hyderabad Metro Rail Limited has submitted Phase II plans covering 162.5 km across eight corridors, including routes from Raidurg to Kokapet Neopolis (11.6 km) and Nagole to Shamshabad RGIA (36.8 km). Estimated combined investment: approximately ₹43,848 crore.

These routes matter because they're connecting employment clusters to residential zones that were previously considered peripheral:

- Kokapet: Residential prices averaged ₹11,512 per sq ft in 2025, up from ₹10,433 in 2024 — a 10% annual increase driven by Grade A commercial proximity and metro pipeline expectations

- Narsingi: Average prices reached ₹10,249 per sq ft in 2025, with absorption remaining healthy despite supply additions

- Adibatla: Capital values at ₹4,650 per sq ft in Q3 2024, still early-stage relative to western corridors — representing the infrastructure-ahead-of-price dynamic that mid-horizon investors track

- South Hyderabad (including Shamshabad): Sales absorption rose 122% in 2024 despite a 58% reduction in new launches — a supply-demand imbalance that typically precedes price acceleration

The Financial District Effect

The Financial District now accounts for 21% of Hyderabad office leasing (H2 2025). Combined with HITEC City, these two nodes absorbed 86% of new office supply in that same period. Key leasing metrics from 2024 underscore how concentrated this demand has become:

- Hyderabad's total office leasing hit 12.5 million sq ft in 2024, its first double-digit annual demand year

- The Financial District alone drove outsized residential absorption in adjacent Kokapet and Nanakramguda

- Grade A commercial leasing concentration is the single strongest predictor of residential price appreciation across Hyderabad's western corridors

For investors tracking the next appreciation cycle, the question is no longer whether the Financial District will continue to anchor western Hyderabad — it's which adjacent residential pockets will capture the spillover demand as core supply tightens.

Trend 3: Luxury Living and Lifestyle-Integrated Real Estate on the Rise

The product that dominated Hyderabad's market a decade ago — the functional, mid-market apartment — is no longer what buyers want or what developers are building.

The Numbers Tell the Story

- Homes priced above ₹1 crore accounted for 62% of Hyderabad sales in H1 2024, up from 42% in H1 2023

- By H2 2025, that share had climbed to 71% — a 29-percentage-point shift in two and a half years

- In Q3 2024, 77% of new launches in Hyderabad were in the high-end and luxury segment (priced above ₹80 lakh)

These numbers point to a structural shift in who is buying and what they're willing to pay for — not a demand spike that will correct itself.

What Buyers Are Actually Asking For

The post-pandemic recalibration of work and home life has made lifestyle integration a genuine purchasing criterion, not a marketing add-on. Buyers — dual-income IT households in particular — are evaluating residential projects on:

- Co-working spaces within the complex (reducing commute pressure during hybrid work days)

- Crèche and childcare facilities built into the development

- Wellness zones, fitness infrastructure, and community services

- Security, housekeeping, and facility management quality post-handover

Developers winning in Hyderabad's premium corridors are building these features in from the design stage, informed by customer research rather than intuition. Evidence-based product design (focus groups, lifestyle mapping, buyer interviews shaping unit configurations) is becoming standard practice among serious players.

As Ashwinder R. Singh has emphasized: technology and data analytics must drive every stage of the process. Smart buildings and personalized services aren't aspirational add-ons — they're the output of that discipline applied consistently.

Trend 4: Technology and Data-Driven Development Raising Industry Standards

Buyers in Hyderabad's premium segment have a straightforward requirement: deliver what you promised, when you promised it. Technology is how leading developers are meeting that bar.

Construction Tech and Delivery Predictability

Tools like Building Information Modelling (BIM) and digital twins are moving from pilot programmes to standard practice among Hyderabad's serious developers. The value isn't just technical — it's commercial. 98% of homebuyers in India demand timely project completion assurance, according to ANAROCK's Homebuyer Sentiment Survey H1 2025. Developers who can demonstrate delivery predictability have a genuine competitive advantage in a market where trust is still being earned.

CREDAI's 2024 report projects accelerated integration of AI, machine learning, and automation across Indian real estate construction — trends already visible in Hyderabad's Grade A residential pipeline.

Data Analytics Replacing Intuition

The more consequential shift is upstream: at the product design and launch timing stage. Developers are increasingly running granular market-fit studies before committing to land acquisition or launch, covering:

- Which unit sizes will sell in a given corridor

- At what price point demand is strongest

- How absorption rates vary across micro-markets

This matters because Hyderabad is not a monolithic market. Adibatla and Kokapet have different buyer profiles, price sensitivities, and absorption rates. Getting the product wrong in either location is expensive — and data analytics is precisely what separates disciplined developers from those relying on instinct alone. That same data-driven mindset is now extending beyond project launch into how communities are managed post-handover.

Smart Communities as the Next Differentiator

AI-enabled facility management is emerging as the post-handover value proposition that distinguishes Hyderabad's premium developments. This includes predictive maintenance, integrated security systems, and app-based resident services.

Singh has stated directly that technology is "no longer an option — it is the new cement of real estate," with smart buildings and personalised services as the tangible output of that philosophy.

What's Driving These Real Estate Trends in Hyderabad

Hyderabad's real estate momentum has specific structural causes. Understanding them helps separate the durable from the cyclical.

Talent and Economic Fundamentals

Telangana's economic data tells a clear story:

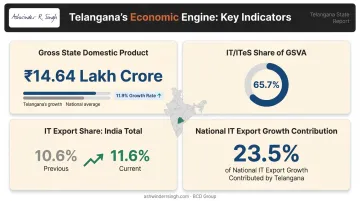

- GSDP reached ₹14.64 lakh crore in 2023-24, growing at 11.9% — well above the national average

- Services account for 65.7% of GSVA, anchored by IT/ITeS

- IT export share rose from 10.6% to 11.6% of India's national total

- Telangana contributed 23.5% of national IT export growth, expanding at 17.93% versus the sector's 8.09% national rate

This economic output directly funds housing demand. Higher incomes produce buyers with stronger purchasing power — and Hyderabad ranks among India's strongest markets on this measure.

Progressive Policy and Planning Framework

Mumbai's restrictive FSI creates acute land cost pressure passed directly to buyers. Bengaluru's standard residential FAR starts at 1.75 and scales by plot size. Hyderabad's building rules framework takes a different approach — road-width, height, setback, and TDR controls give developers more flexibility in density management.

That flexibility translates to a lower per-unit land cost burden and more room to deliver quality at competitive price points.

Inventory Management: A Mixed Picture Worth Watching

Hyderabad's inventory overhang stands at 24 months as of Q1 2025, the highest among India's top 7 cities. This compares to 11 months in Bengaluru and 15 months in Mumbai. For buyers, this means negotiating power and product choice. For investors, it suggests absorption must be monitored — the market is not undersupplied, and projects without strong location or product differentiation will take longer to sell.

Competitive Positioning vs. Peer Cities

Relative to Mumbai (extreme land scarcity, high entry price), Bengaluru (infrastructure stress, higher rental yields but traffic congestion), and Delhi NCR (regulatory complexity, slower RERA maturity), Hyderabad offers a coherent combination:

- Lower base prices with comparable or better rental yield potential

- Transparent RERA-governed transactions

- Strong infrastructure investment signalling from the state government

- GCC and IT sector diversity reducing single-employer concentration risk

For a rigorous framework to evaluate and compare real estate markets across India, Ashwinder R. Singh's Master Residential Real Estate and A to Z of Residential Real Estate provide step-by-step investment selection methods built from hands-on market experience.

How These Trends Are Reshaping Opportunities for Buyers and Investors

For Homebuyers

Buyers entering Hyderabad today benefit from:

- Delivers premium construction quality — technology-enabled builds and lifestyle-integrated design are now standard in new launches

- Offers relative affordability — entry prices remain lower than Mumbai or Bengaluru for comparable specifications

- Provides regulatory clarity — RERA-governed transactions reduce documentation and title risk significantly

That said, due diligence still matters: micro-market selection (don't treat Hyderabad as homogeneous), clear land title verification, and developer track record on previous handovers.

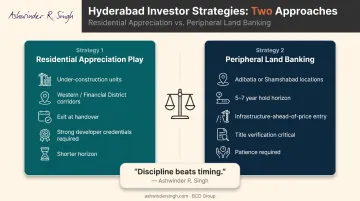

For Investors

Two primary strategies are relevant to Hyderabad's current market cycle:

- Residential appreciation play: Buy under-construction units in high-demand western and Financial District corridors, with exit planned around handover. Works best with strong developer credentials and clear infrastructure proximity.

- Peripheral land banking: Acquire land in corridors like Adibatla or Shamshabad with a 5–7 year hold horizon, ahead of infrastructure delivery. Requires deep title verification, clear local governance understanding, and patience.

Singh's investment philosophy — "discipline beats timing" — applies here. The investors who have done well in Hyderabad are those who bought sound assets in credible corridors and held through cycles, rather than trying to time entry and exit around sentiment.

For Developers

Customer expectations have fundamentally reset. What once differentiated a developer now defines the minimum bar for market credibility. Developers who haven't invested in these areas are already losing ground:

- Customer-centric design that reflects how residents actually live

- Data-informed product calibration aligned to micro-market demand

- Technology-enabled delivery with transparent project tracking

- Post-handover service quality that sustains buyer trust long-term

The developers gaining share are those who built these capabilities proactively — not as a response to competition, but as a reflection of where the market was heading.

Future Signals: What to Watch in Hyderabad Real Estate

GCC Expansion Beyond Existing Clusters

Hyderabad hosts over 355 GCCs as of 2025, employing over 300,000 professionals and contributing 12% of India's GCC talent pool. Telangana's stated target is 500+ GCCs by 2030, with 27 new GCCs launched in Hyderabad in H1 2025 alone.

Currently, 80% of GCCs are concentrated in HITEC City, Financial District, and Genome Valley. As those zones price up, peripheral corridors will become viable GCC locations, creating new residential demand pockets further out from the core.

NRI Investment Flows

India-wide, NRI investments in real estate were forecast to contribute 20% of total transactions by 2025, with over 25% of NRI buyers targeting budgets above ₹1 crore. Hyderabad is well-positioned to capture a disproportionate share of those flows, driven by several structural advantages:

- A large Hyderabadi diaspora concentrated in the US and Middle East

- RERA-governed transaction transparency that reduces long-distance risk

- Rupee-denominated returns that benefit from currency dynamics

- Strong familiarity with the city among second-generation NRI buyers

Scenario Outlook for 2025–2027

| Scenario | Conditions | Likely Outcome |

|---|---|---|

| Base case | Metro delivery on track, IT hiring stable | Well-connected corridors outperform city average on price appreciation |

| Upside | GCC expansion accelerates, NRI inflows surge | South and peripheral corridors reprice faster than expected |

| Risk | Infrastructure delays, FSI policy changes, or macro slowdown | Absorption moderates; inventory overhang at 24 months becomes a constraint |

The 24-month inventory overhang is the primary risk factor to watch. It doesn't signal a market breakdown. What it does signal is that projects launching over the next 12–18 months need metro-adjacent positioning, ticket sizes below ₹1.5 crore, and genuine amenity differentiation to move inventory at pace.

Frequently Asked Questions

Which area is best for real estate in Hyderabad?

The Financial District, Gachibowli, Kokapet, and Narsingi consistently rank as the top zones, combining IT employer proximity, strong infrastructure, and high absorption. The "best" area depends on your budget, whether you're buying to live or invest, and your hold horizon — there's no single right answer.

Is Hyderabad real estate a good investment in 2025?

Hyderabad's strong employment base, progressive planning policy, and affordability relative to Mumbai and Bengaluru make it one of India's more credible investment markets for medium-to-long holds. The 24-month inventory overhang is worth watching, but it doesn't outweigh the structural positives.

What is driving property price appreciation in Hyderabad?

The primary drivers include:

- IT and GCC sector employment growth

- Dual-income household formation

- Infrastructure investment (metro, ORR, commercial corridors)

- Supply constraints in premium zones

- Growing NRI and institutional capital inflows

How does Hyderabad compare to Bengaluru and Mumbai for real estate investment?

Hyderabad offers lower base prices and more developer-friendly FSI, though Bengaluru leads on rental yield at 4.45% vs. Hyderabad's 3.3% (Q1 2024). Mumbai delivers greater liquidity; Bengaluru offers higher speculative upside in select tech corridors. Hyderabad's edge is structural affordability backed by IT-driven job creation.

Are NRIs investing in Hyderabad real estate, and why?

NRI investment in Hyderabad has grown steadily, driven by city familiarity among the US and Middle East Hyderabadi diaspora, attractive rupee-denominated returns, and RERA-backed transaction transparency. The city's long-term expansion trajectory — anchored in IT sector growth and GCC proliferation — reinforces the case.